As we are now a few days into the new tax year, and you are starting to think about getting your return information together, we thought it would be the perfect opportunity to remind you of what is ‘allowbable’ when working out your taxable profits for the year.

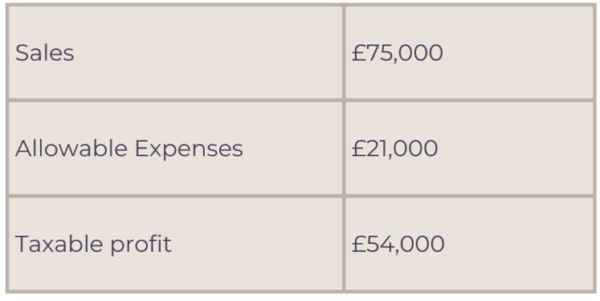

Example

Tax is charged on your taxable profit, so it is important that you, as a self-employed individual, understand which costs you can deduct from your revenue before your tax bill is calculated.

What are the general rules?

- For something to be an allowable expense, it must be ’wholly and exclusive’ for business purposes

- When a transaction is both business and personal, a deduction is allowed for the portion that is used for business-related reasons. For example, if you use a mobile phone and 50% is used for business, you will be able to deduct 50% of your phone bills from your revenue.

- When a personal expense is made, that is not related to the running of your business, these are never allowable for tax purposes.

Trading allowance

If you have expenses under £1,000, you are entitled to claim the ‘trading allowance’ which is a fixed £1,000 that will be deducted from your revenue before your taxable profit is calculated.

Note : you cannot claim any other expenses if you include this allowance in your computation. You are also unable to claim capital allowances on asset purchases.

Simplified expenses

To avoid complicated calculations for costs that have both business and personal use you can use flat rates provided by HMRC for vehicles, working from home or living on your business premises.

- Vehicles: 45p per business mile for the first 10,000 miles in the year and 25p per mile after that. Once you use this flat rate method for a vehicle you must continue to use this way moving forwards.

- Working from home: see below for the monthly cost you can claim depending on the amount of hours that you work from home.

-25-50 hours per month £10

51-100 hours per month £18

more per month £26

- Living at your business premises, for example, if you run a guest house use the below flat rates to deduct your fixed personal costs from the total expenses of the premises

1 person living there £350 per month deduction

2 people living there £500 per month deduction

3+ people living there £650 per month deduction

Capital allowances

When buying something big for your business that has an expected useful life of more than a year, you’ll claim capital allowances on this cost.

- Annual Investment Allowance: 100% of the cost in the year of purchase, can be claimed on qualifying plant and machinery such as commercial vehicles, electric cars, equipment or computers.

- Writing down allowances: 18% or 6% of the cost each year, can be claimed on cars or plant and machinery that does not qualify for AIA – this can be a complex area so do reach out if you have any questions.

Cash-basis system

This can be used if you are a sole trader with an income of £150,000 or less. This means you can only account for income when you receive it and expenses when you pay them.

- A simpler method, however, may not be the best option for more complex businesses or ones that need financing, since banks usually prefer traditional accounting.

- With this, you can claim expenses for day-to-day business costs, things you resell, and big items like machinery, computers and vans. You can only claim £500 in finance and interest charges, and you can’t use losses to offset other income.

Allowable expenses

Office costs, travel, clothing, staff, goods for resale, financial costs, property expenses, advertising, and training – all count as allowable expenses.

But what does this mean?

Don’t worry, we’ve broken down it for you below! The below is not meant as an exhaustive list but to give you examples of both allowable and non-deductible expenses that you may incur.

Office costs

- Stationery, rent and rates, computer software, power, and insurance

Car, van, and travel expenses

- Vehicle insurance, repairs and servicing, fuel, parking, hire costs, breakdown cover, bus, air and train fares, hotel costs and subsistence on business trips all count as allowable expenses.

- Non-allowable: Parking fines, non-business driving expenses and travel between home and work.

Clothing

- The costs of everyday clothing are not able to be claimed, even if worn within the business, however, the likes of uniforms, branded items, protective clothing and costumes for entertainment are allowed.

Staff costs

- Staff costs are allowable; however, carers and domestic help are not allowed.

Goods for sale

- Stuff you buy to resell, like raw materials or the cost of making goods, can be claimed as allowable expenses.

- You cannot claim depreciation on equipment, but you can claim the cost through capital allowances.

Legal and financial expenses

- Legal fees, accounting costs, charges for architects or surveyors, as well as premiums for professional indemnity insurance.

Marketing and subscription costs

- Advertising, free samples, website costs, trade journals, and professional memberships linked to the business.

- Non-allowable: Political donations, gym memberships (unless provided to all staff and a P11d completed), charity donations (not including sponsorships), and hospitality for clients or suppliers.

Training costs

- Allowable expenditure includes training to improve skills, updating knowledge and improving skills to support the business.

Claiming allowable expenses

So now you know what is and isn’t an allowable expense, how do you claim them?

Records, receipts, and invoices need to be kept safe to support allowable expenses.

The total of allowable expenses can be claimed on a self-assessment tax return, while proof of spending does not need to be submitted with the return, it should be retained in case of an HMRC query.

If you need to comply with Making Tax Digital for Income Tax you will need to be reporting your income and expenses quarterly from 6th April 2026. Please check out our blog post on this if you are unsure if this applies to you.

For any other questions on what is allowable and what isn’t, feel free to give us a call on 01872 267 267, email us contact@whyfield.co.uk, or message us on WhatsApp 0777 49 39 111